The Committee for A Responsible Federal Budget (CRFB) calls the most recent budget deal expected to be passed by the Senate and signed into law by President Donald Trump this week “The Worst In History.”

That is saying something. There have been plenty of budget deals that were flat-out terrible. All the bad ones increased deficits dramatically and, therefore, our national debt. Only a few — the 1990 Budget Agreement and the 1997 Balanced Budget Act mainly — did anything to arrest the steady inexorable climb to $22 trillion in debt today.

Elected politicians used to at least try to give credence to their claims they were serious about “balancing the budget.”

Now they don’t even try anymore.

According to CRFB:

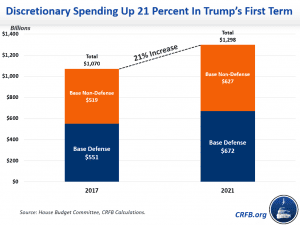

- President Trump and Congress will have increased discretionary spending by 21 percent over his first term insuring annual trillion-dollar deficits into law for a long time.

- President Trump said after signing the 2018 omnibus bill that exploded discretionary spending that he would “never sign another bill like this again.”

- Republicans used to insist that a dollar of spending had to be cut for every dollar increase in the debt limit.

Before that, in the 1990s, a majority in Congress made up of Republicans and Blue Dog Southern Democrats forced Congress and President Bill Clinton to abide by the following simple rule of PAYGO (pay-as-you-go):

- For every dollar of increase in new domestic or defense spending, a dollar had to be cut in some other existing program.

- For every dollar increase in new proposed entitlement spending, a dollar in a new tax had to be raised on someone to pay for it.

- For every dollar in new tax cuts, a dollar had to be found in savings in entitlement programs through budget reconciliation legislation to make it “budget-neutral.”

The cardinal rule to climb out of any financial hole is to stop digging the hole deeper first. That means stop spending more money on expanding existing programs or starting new ones which Presidents Bush 43, Obama and now Trump, along with complicit members of Congress and Senators have failed to do for the past two decades.

Ross Perot, who recently passed away, ran for president in 1992 and 1996 as an independent. He was famous for two things: “The giant sucking sound you hear is jobs going to Mexico because of NAFTA!” and, essentially, “It is the national debt, stupid!”

He did not win a single electoral vote. He did draw national attention to the dangers of never balancing the federal budget. A Republican Congress worked with President Clinton’s chief of staff, Erskine Bowles of North Carolina, to pass the Balanced Budget Act of 1997 that birthed the only four budget surpluses we have seen in most of our lifetimes.

Perot helped make voters ready to listen to federal spending restraint.

Are we going to wait for another economic calamity such as what we experienced from 2008-10 to get our fiscal house in order? Everyone thought that catastrophe was going to trigger an era of fiscal sanity.

They were wrong; President Obama and the Democratic Congress from 2009-11 went on an orgy of spending that put any real orgy in ancient Rome to shame.

Where are our brave and smart elected members of Congress and senators who understand budgets, economics and who can count? Why don’t they produce a budget that 218 representatives in Congress and 51 senators can support to save us from this colossally stupid build-up of debt, the largest America has ever amassed in peacetime?

Who is going to be the next “Ross Perot” 2020 at either the congressional, Senate or presidential level?

(first published in North State Journal 7/31/19)

Do You Want Better People to Run for Public Office?

Support the Institute for the Public Trust Today

Visit The Institute for the Public Trust to contribute today

Support the Institute for the Public Trust Today

Visit The Institute for the Public Trust to contribute today

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.